The Best Crypto Cards for Digital Nomads in 2026 (and Why Revolut, Wise and N26 Shouldn't Be Your Base)

Updated July 3, 2026

Photo: working from the beach, by AbhiSuryawanshi / Wikimedia Commons, CC BY-SA 4.0.

{kind=link}

The best base card for a digital nomad is one no single company can freeze while you're a continent away from support. Revolut, Wise and N26 are fine as backups, but each locks accounts for compliance reviews with little warning. A crypto card you fund yourself, with no FX fee and stablecoin support, keeps control in your hands and pays cashback on top.

Updated July 2026

Picture the moment it goes wrong. You're six weeks into a stretch in Bali, rent falls due on the first, and a client just wired the biggest invoice of your quarter. You open the app to pay your landlord and the balance won't move. A grey banner mentions a "routine review." The chat hands you to a bot, then a queue, then a promise that someone will email within "up to 10 business days." Your landlord wants cash today, and your card gets declined at the ATM on top of it. This happens to nomads all the time, and it's the exact reason I stopped trusting one app to hold all my money.

What actually happens when a neobank freezes you

Let me be fair first. Revolut, Wise and N26 are good products. Fast transfers, honest mid-market rates, a clean app. I still keep one. The trouble starts when their automated systems see something they don't like: a login from a new country, a large incoming transfer, a spending pattern that trips a model you can't inspect. They freeze the account first and review it afterwards, and "afterwards" runs on their clock, not yours.

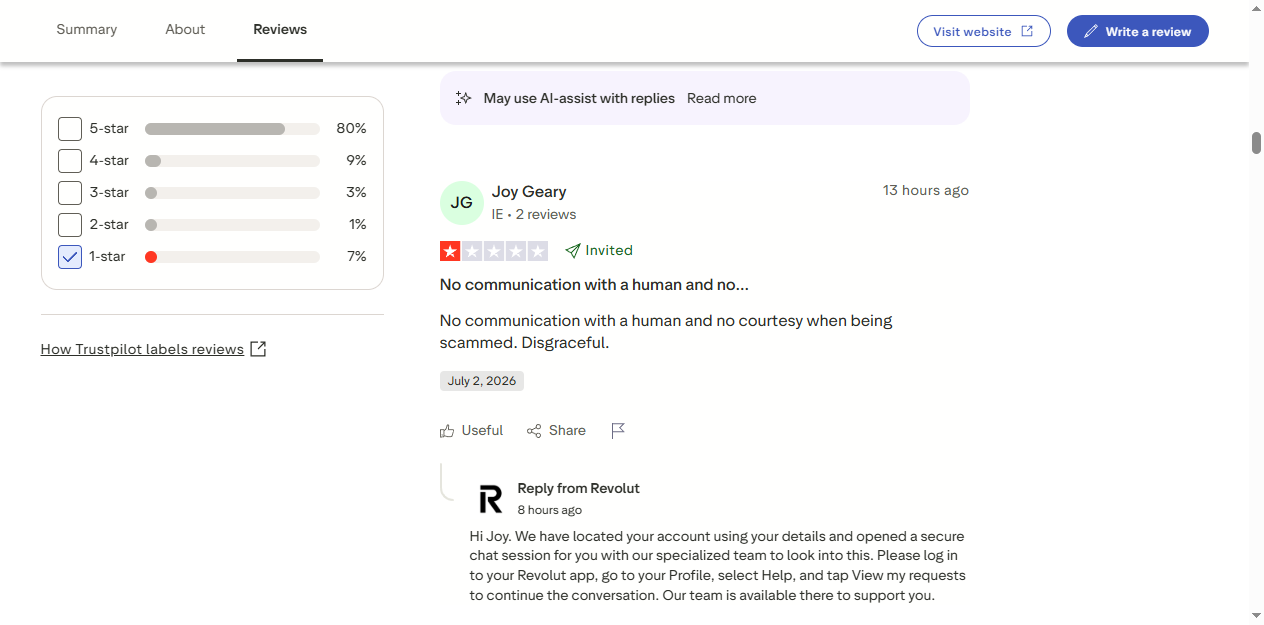

Read the one-star reviews and the same scene repeats. One Revolut customer describes an account "locked for an internal review," no access to their money for days, no explanation and no timeline. Another watched Revolut block their outbound transfers to a different bank, then route them through an AI chatbot before a human finally said, in so many words, "I can't do anything, open a complaint at this link." For someone sitting in a cafe in Chiang Mai with a landlord waiting, that isn't a minor bug. It's a week of your life and your rent held hostage.

None of this shows in the headline number. Revolut sits at 4.7 on Trustpilot, and most months it works fine. Filter to the one-star reviews though, roughly 7% of 421,000, and the theme is unmistakable. The problem isn't that these apps are bad. The problem is concentration. An app that can pause your access on a model's hunch is acceptable as a backup. As the only way you reach your money, 8,000 km from the nearest branch, it's a single point of failure you have no reason to accept.

The nomad rule

Never let one account hold all your access to money. If a single freeze can strand you in another country, your setup is too fragile. The fix isn't a better bank. It's spreading the risk so no one company owns your off switch.

Why a crypto card makes a better base

A crypto card changes who holds that off switch. Your money sits in your own wallet or on an exchange you chose, and the card pulls from it only at the moment you spend. No neobank sits in the middle deciding whether today is the day your rent clears. The better cards also kill the fee that quietly drains a nomad's budget more than any other: the foreign-exchange markup.

Run the numbers on that markup, because it's bigger than it looks. Say you spend €3,000 a month across rent, food and the odd flight while hopping between currencies. A 2% FX fee on that is €60 a month. That's €720 a year handed to a line item you never see itemised on a statement. A zero-FX card gives it back. Layer 1 to 2% cashback on top and a good crypto card can genuinely cost you less than nothing to run.

The cards I'd actually carry

Gnosis Pay: for keeping full control

Gnosis Pay is the closest thing to a self-custodial bank account on the market. It's a Visa that spends straight from an on-chain wallet you control, with no FX fee, no monthly fee and an IBAN in the EU. Your euros sit in EURe, a euro stablecoin, until the second you tap. No company can freeze a balance it never holds, which is the entire point. The catch: setup asks more of you than a normal app, and it leans EU-first. If self-custody is your priority, the extra ten minutes are worth it.

Rain: for living in your web3 wallet

Rain is a self-custodial Visa that spends from the web3 wallet you already use, with no exchange account, no FX fee and 1% back in ETH. If your money already lives on-chain and you just want to spend it without moving it through a middleman, Rain is the least friction of the lot. Email-only sign-up keeps the start quick.

ether.fi: for making idle money work

The ether.fi Card earns restaking yield on your balance while it sits there, then pays 2% back in ETH when you spend, with zero FX fee. It's the pick for nomads who want their float earning instead of gathering dust between paydays. It asks for full KYC, so set aside an afternoon for verification before you rely on it.

Kast: for starting today, no ID

Kast issues a virtual Visa with no KYC that you load with USDT or USDC and spend worldwide. It's the fastest way to get a working card in a single afternoon, and the privacy is real. Two trade-offs keep it out of the top spot: a 2% FX fee and no cashback, so it fits smaller day-to-day spending rather than your rent. If privacy is the goal, compare it against our full no-KYC card list before you commit.

The high-cashback names, with an asterisk

You'll see Crypto.com advertise 5% and Binance flash up to 8%. Read the fine print before you get excited. Those headline rates need you to stake a large pile of the provider's own token, and the reward collapses without it. Binance carries a second problem for anyone in Europe: it reached the MiCA deadline without an EU licence. A platform that can restrict or freeze access is exactly the risk this whole article is trying to design around. Fine cards to hold on the side. Not the ones I'd build a nomad life on.

Compare the full nomad shortlist

The three-layer setup that won't strand you

Here's the structure I run and recommend to anyone going long-term. Three layers, so no single failure can leave you stuck at a market stall with a dead card.

- Layer 1, the vault. The bulk of your money, the part you won't touch this month, stays in your own wallet or on a licensed exchange. Cold, boring, untouched.

- Layer 2, the spender. Two or three weeks of spending, held in stablecoins on a crypto card. This is what taps for rent, groceries and flights day to day.

- Layer 3, the backup. One traditional card, Wise or Revolut included, carrying a small float. You use it when a merchant refuses your main card, and you never depend on it.

If layer 2 gets declined at a night market, layer 3 covers dinner. If a neobank freezes layer 3, you shrug and keep moving, because it was never holding much. That redundancy is the whole game. The goal isn't to find one perfect card. It's to make sure no single company can ruin your week.

Find your nomad card

Answer 5 questions and we'll match a card built for low fees, high limits and life on the move.

Frequently asked questions

There's no single winner, because it depends on what you value. For self-custody, Gnosis Pay lets you spend from a wallet you control with no FX fee. For a quick no-ID start, Kast issues a virtual card in an afternoon. For yield on idle funds, ether.fi earns restaking rewards while you spend. All beat leaning on one neobank that can freeze you.