The Best Crypto Cards in the Netherlands (2026)

Updated July 3, 2026

The best crypto cards in the Netherlands compared on fees and cashback, plus how the Belastingdienst taxes crypto under box 3.

Updated July 2026

The Netherlands sits inside the EU and the eurozone, so you get the full European card set without any of the friction that hits people in smaller markets. This is also home turf for MiCA-licensed exchanges. Bitvavo in Amsterdam holds a licence under the new EU rules, which means the on-ramp from euros into crypto and back again works cleanly, and the cards that plug into that flow behave the way you expect. If a provider issues a euro IBAN and runs on Visa or Mastercard, a Dutch resident can use it the same day it goes live across the continent.

One thing catches almost everyone off guard here. The Belastingdienst does not tax your crypto as a capital gain when you spend or sell. It taxes your holdings as wealth under the box 3 system, based on what you own on 1 January each year. That single detail changes how you should think about a card. In most countries every tap is a taxable event you have to log. In the Netherlands the tap itself is not the trigger. You still keep records, and you still confirm your own situation, but the mental model is different from what you read on American or British sites. I will come back to this below because it matters more than the cashback rate.

The best crypto cards in the Netherlands

| Card | Network | KYC | Cashback | Best for |

|---|---|---|---|---|

| Gnosis Pay | Visa | Yes | 2% GNO | Self-custody with a euro IBAN |

| Nexo | Visa credit | Yes | 2% BTC | Spending without selling |

| Crypto.com Visa | Visa | Yes | Up to 5% CRO | High spenders who stake |

| Wirex | Visa | Yes | 2% WXT | Multi-currency travel |

| ether.fi | Visa | Yes | 2% ETH | ETH holders earning yield |

| MetaMask | Mastercard | Yes | 1% | Web3 natives |

| ZEN | Mastercard | Yes | Up to 10% merchant | Euro banking plus rewards |

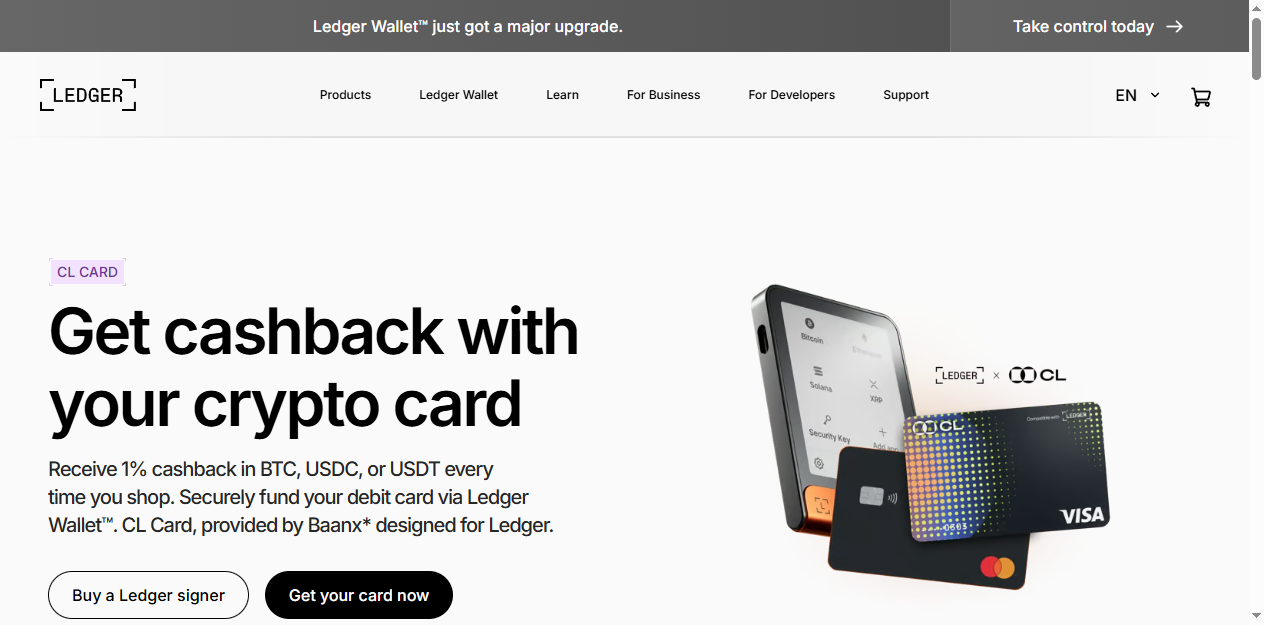

| Ledger CL | Card | Yes | 1% | Ledger hardware wallet users |

| Bybit | Card | Yes | Up to 3% | Exchange users, MiCA via Austria |

| RedotPay | Visa prepaid | Yes | Varies | High limits |

| Bitsa | Visa prepaid | No | Varies | Privacy, no KYC |

Crypto cards available in the Netherlands, live from our data

Gnosis Pay, the self-custody pick with a real IBAN

This is the one I point Dutch friends to first. Gnosis Pay is a decentralised Visa card that stays non-custodial, so your funds live in a wallet you control rather than on some company balance sheet. You get an EU IBAN backed by EURe, a euro stablecoin, which fits the Dutch setup perfectly. FX is 0, cashback runs at 2% in GNO, and because it settles from your own account you keep the custody story clean. For anyone who cares about holding their own keys, nothing else on this list comes close.

Nexo, spend the value without selling the coins

The Nexo card is a Visa credit card that lets you borrow against your crypto rather than sell it. You keep the upside of your holdings and spend a credit line secured against them. Cashback is 2% in BTC, and it comes with an IBAN. Given the box 3 system here, where selling is not the taxable moment anyway, the appeal of a borrow-and-spend card is less about tax and more about keeping your position intact. Still a strong tool if you believe in your bags.

Crypto.com Visa, best if you spend big and stake

The Crypto.com Visa runs 0 fees and 0 FX, which already puts it ahead of most bank cards for travel. Cashback climbs to 5% in CRO, though the higher tiers need a stake, so read that carefully before you lock anything up. Airport lounge access sweetens it for people who fly out of Schiphol often. If you spend real money each month and do not mind staking, the numbers work in your favour.

Wirex and ether.fi, two specialists worth a look

Wirex carries 0 FX, 2% WXT cashback, and support for more than 40 currencies, which makes it a natural travel card for anyone leaving the eurozone. ether.fi stays non-custodial with 0 FX and 2% ETH cashback, and it layers restaking yield on top, so your idle ETH keeps earning while it backs your card. Pick Wirex for the road and ether.fi if your whole thesis is ETH.

The rest of the field

The MetaMask card is a non-custodial Mastercard with a free virtual option, 1% cashback, and 0 FX, which suits people who already live inside a Web3 wallet. ZEN is a Mastercard from an EU EMI that pairs a euro IBAN with merchant cashback of up to 10%, a solid all-rounder for daily banking. The Ledger CL funds straight from your Ledger wallet and pays 1%, ideal if your hardware wallet is already the centre of your setup. Bybit offers up to 3% cashback and runs its MiCA licence through Austria. RedotPay is a Visa prepaid card with high limits, and Bitsa is a no-KYC prepaid Visa available across the EU for those who want privacy.

Dutch tax and the euro setup

- The Belastingdienst taxes your crypto holdings under box 3, as part of your wealth measured on 1 January each year, rather than taxing each spend or sale as a gain.

- This differs from most countries, where every disposal is a capital gains event you have to calculate. Here the value you hold on the reference date drives the bill.

- Keep records anyway. You still want a clear picture of what you held and when, both for your own filing and for any questions from the Belastingdienst.

- An EU IBAN is standard in the Netherlands, so favour cards that issue one. Gnosis Pay, Nexo, and ZEN all give you a euro account you can top up by SEPA transfer.

- Favour 0% FX cards. Inside the eurozone you rarely pay conversion, but the moment you travel outside it a 0 FX card like Crypto.com, Wirex, or ether.fi saves you real money.

- Confirm your own position with a Dutch tax adviser before you make decisions. Box 3 rules have shifted in recent years and your situation may differ from the general picture.

Compare every crypto card available to Dutch residents

Frequently asked questions

No, not in the way people expect. The Belastingdienst taxes your holdings under box 3 as wealth on 1 January, not each transaction as a capital gain. The spend itself is not the taxable trigger. Keep records regardless, and check your own case with a Dutch tax adviser, because the general rule may not fit every situation.